As an SME business owner you may have an immediate or short term cash requirement, such as the opportunity to acquire stock the next day or a new job/project that requires short term funding.

But approaching your bank may not be an option for a speedy cash flow solution because banks have to go through all kinds of hurdles to approve a loan. Quite often it can take several weeks or longer to get a loan from a bank.

Recently there’s been a substantial increase in sophisticated fintech lenders who are transforming the financial landscape with new technology and innovation.

You may be sceptical of fintechs to begin with, and while they’re not for everyone, new fintechs are now reputable and well funded. Opportunity-wise they can offer a great solution if you need quick funding.

Benefits of fintechs

There are now a wide range of fintechs. Some banks have a vested interest in them so they can capitalise on the technology they provide. They are also owned by peer-to-peer lenders, hedge funds or private equity funds.

Benefits of using fintechs include:

- Fixed-term, unsecured loans

- Speedy lending and efficiency of process

- They don’t need security other than a directors’ guarantee

- They can be used for urgent or short term funding

- Decisions are made within 48 hours, settlement in as little as 24 hours

- Don’t have masses of documentation, it’s all done online.

Also, for SMEs who have an urgent requirement and have security, unsecured business finance with a fintech could be a lead-in (i.e. you can then refinance with another lender/bank later).

Fintechs – what you need for unsecured business finance

If you’re fully transparent unsecured loan with a fintech can be a great solution.

Depending on who you go to, fintech lenders typically want to see an SME’s cash flow through their most recent bank statements (e.g. 6 months), plus up-to-date management and ATO accounts. As a lender they need to know that a business can generate cash flow to repay the loan.

They feed your electronic data into an algorithm, which analyses it, and allows them to assess it quickly.

Scenario: Applying for a fintech loan to buy stock

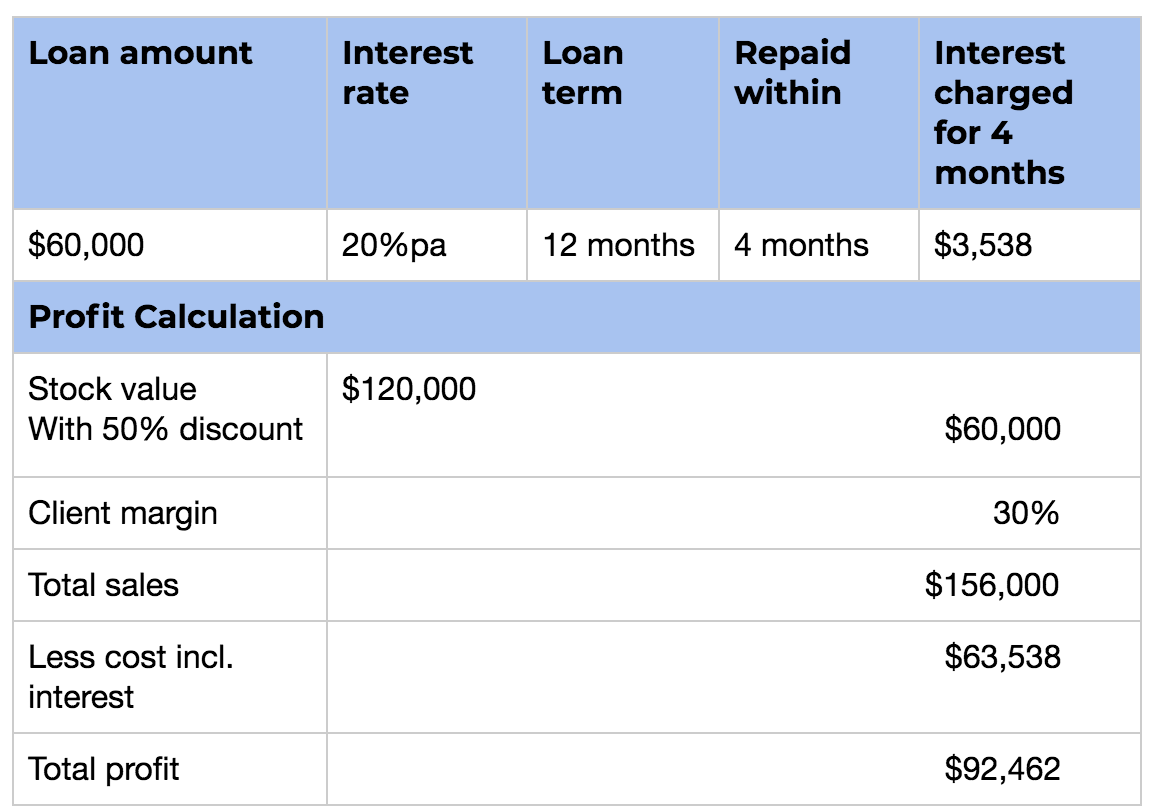

An SME business owner had the opportunity to buy an amount of stock at a 50% discount if they paid for it the next day. Their bank’s turnaround estimate was 4-6 weeks for a decision, and that included updated valuations plus a formal review, plus multiple layers of credit approval.

The client’s finance broker suggested he consider one of the fintechs, which the Broker approached on the client’s behalf. At 8.30am in morning he loaded the data with the fintech online requesting a $60,000 loan (attracting a 20% interest rate). The loan was approved by noon. The client accepted the documents the same day, settlement occurred the next day and funds were immediately transferred on the same day as the settlement.

As shown in the table below, the client repaid the loan within 4 months and so the cost of interest was approximately $3,500 for that period. But the profit he made on the stock, as well as discount he received, more than offset the higher interest rate he paid the fintech lender. Overall the client made approximately $92,000 from the transaction, therefore, the $3,500 interest cost was nominal to him.

In this case immediacy was necessary. He may have lost the opportunity if he waited 4-6 weeks for a bank to approve the loan.

Final Thoughts

The pace of unsecured business lending is increasing substantially, with fintech lenders becoming more sophisticated and offering SMEs a wide range of quick and easy, pain free products. So don’t let an opportunity pass you by just because financing seems too hard. A smart finance broker will help you assess what’s suitable, so speak with them about all the unsecured business finance options available.